Why Maple Finance's Milkshakes Will Bring All the Boys (Banks) to the (DeFi) Yard

Why Maple Finance's Milkshakes Will Bring All the Boys (Banks) to the (DeFi) Yard

Yeah, I can't believe this is the name of my first article either.

While the TVL across DeFi protocols has ballooned from ~$1bn in the summer of 2020 to $200bn+ today, that figure is peanuts compared to the lending businesses and capital needs of institutional companies; those bulge-bracket banks like JP Morgan and Goldman Sachs. Maple Finance is a DeFi protocol aiming to lay down the decentralized rails for capital markets, with the goal of eventually bringing this institutional capital on-chain. The protocol brings sorely needed undercollateralized lending to DeFi and crypto, while maintaining the strict risk control and compliance requirements critical in the traditional finance world. This unique combination, via a surprisingly simple platform design, will see Maple Finance as a top-10 dapp by TVL by the end of 2022.

Background

Disclaimer: nothing in this article is financial advice, I have no association with Maple Finance apart from owning some MPL tokens and being a big fan of the protocol.

This is not meant to be a deep technical dive into Maple, or a step-by-step guide on how to use it, but rather a look at why the team’s design choices represent, in my opinion, the first DeFi protocol that has a real shot at attracting institutional capital. A frequently circulated claim on CT (crypto Twitter) is “the institutions are coming”, often used to justify the claimers’ own bullish narratives. What I mean by institutional capital is the existing lending practices of traditional banks (of all sizes, but particularly the bulge bracket banks whose clients include massive corporations, institutions, and even governments). I’m talking about JP Morgan, Goldman Sachs, etc. DeFi holds immense promise for a new economic system that is simply a better version than the one we use today. However, there are material roadblocks that must be overcome before we start to see institutions like those listed making the jump into DeFi.

Debt, Debt, Debt

I thought it would be helpful to quickly address what the term “capital markets” refers to, specifically debt capital markets, to help frame the size of the market Maple is targeting. For the sake of simplicity, I won’t be getting into anything more complex like syndicated debt. This is your standard Borrower-Lender financing. Maple is in its earliest design/phase right now, and will certainly allow for increased flexibility and complexity over time to mimic its traditional counterpart.

I spent a few years after graduating college working as an underwriter at a (relatively) large US bank, mainly focused on lending to tech companies. I understand the frictions and bottlenecks of the traditional credit process. I decided to quit last summer to be a full-time on-chain degen, so I have a perspective on both sides of the system. I’ve been rug-pulled with the best of them, and drowned my sorrows shitposting with the rest of CT while digital asset markets cratered. Seeing both sides is why Maple really stuck out to me - but more on that later.

The term Capital Markets, put broadly, refers to the marketplaces in which two parties do business with one another; one party is in demand of capital (Borrowers) and the other who supplies said capital, at a price (Lenders). Bringing borrowers and lenders together in an efficient way is the entire goal - and capital markets are a core tenet of capitalism and free markets; arguably the single biggest reason that humanity has progressed so rapidly over the last few centuries.

Everybody needs debt. Debt to invest in new equipment for your company, debt to make early-stage investments, debt to finance ongoing operations, etc. The world runs on debt. We’ve been slinging debt for thousands of years, as far back as farmers in Mesopotamia borrowing seeds they would later pay off with that season’s harvests. As global GDP has grown, so too has this demand for debt. Some of the McKinsey’s of the world describe this market as “the capital available for intermediation globally” or “global financial stock” - and it’s nearly impossible to quantify. But it’s in the range of hundreds of trillions of dollars, if not more. There is a future where a large portion of that moves on-chain, but it will take time.

There are, obviously, inefficiencies in the current banking system. But it is easy to see how banks are comfy with the way things sit, as there is little short-term incentive to make massive structural changes in the way they conduct business. Technologically, the financial system is one of the last huge industries to modernize and catch up with the digital age. Sure, you hear about Robinhood, Square and Venmo, but the reality is that most banks are using the same antiquated infrastructure and systems they have been using for decades. Unfortunately, too much of what we see in crypto (especially up until recently, when there weren’t a ton of actual products) is “it’s like blank industry, but on the blockchain, bro”.

In that regard, Maple is far more than just “a corporate credit market on the blockchain”. They have deliberately modeled the platform to tap into the best aspects DeFi without completely forgetting the current system - and that’s why I believe Maple will be the protocol to bring massive amounts of tradfi capital on-chain in the coming years.

Maple Finance Overview

Like most DeFi protocols, at its core Maple Finance offers a suite of open-source smart contracts on Ethereum, accessible via digital wallet. The process of taking out a loan on the blockchain via Maple looks mechanically similar to how you would do so in the current system. In traditional capital marketplaces, the standard actors involved are the Borrower and the Lender. Borrowers are in demand of capital (to finance growth, make investments, whatever it might be) and Lenders have a surplus of capital (looking to earn a return on said capital, versus it sitting idle and unproductive). Maple refers to Lenders/Liquidity Providers interchangeably, but I’ll stick with Lenders throughout.

Pool Delegates

The core change that Maple uses to disrupt this relationship is the introduction of Pool Delegates - they have essentially taken the process of underwriting credit risk (historically done by the Lender themselves) and broken it out independently. This has not been possible in the traditional system for many reasons, but here comes the magic of cryptography and smart contracts to shake things up.

In tradfi, the Lender has some capital on its balance sheet that it can deploy to earn interest, normally via lending. To do so, the bank employs a credit team whose sole job is to determine which Borrowers to lend money to, depending on their creditworthiness. As an underwriter, I was doing mostly grunt work, filling in financials provided by Borrowers to determine if they fit some preordained definition of creditworthiness, which would eventually get sent up through the ranks to a Senior Credit Officer who ultimately decided ‘yes’ or ‘no’ on making this particular loan. There is obviously a ton of nuance to this due diligence process, and it differs drastically depending on the institution and what the Borrower is looking for - but that’s a simpleton’s version of the lending process. This should not be rocket science to anyone reading. The important part is that Lenders are taking on some level of risk when making a loan, and they do everything in their power to minimize this perceived risk. In addition, Lenders are regulated by the government and must abide strictly by these rules, which are mainly designed to limit bad actors/criminals who are seeking banking services.

In Maple’s protocol, Pool Delegates replace these credit teams. Delegates are firms/individuals with years of experience in credit risk assessment and asset management in the tradfi world. In order to be allowed on the Maple platform, the wannabe Delegate must be vetted and approved (whitelisted) by the Maple team, who looks at their background and track record.

Each Delegate manages a single Liquidity Pool, from which loans are issued to prospective Borrowers. But the decisions around which Borrowers to lend to, and at what terms, fall entirely on the Delegate - remember, these are folks with extensive credit backgrounds. Delegates perform due diligence, negotiate terms with the prospective Borrower, and monitor the ongoing health of their Pool’s loan portfolio. In return, Delegates receive a portion of fees earned by their Pool - essentially a performance fee.

There are currently six of these Pools, run by 4 Delegates, on Maple

In traditional finance, a bank’s credit team is not necessarily incentivized beyond the standard performance bonus / desire to be promoted. They aren’t reaping the rewards of their due diligence, which typically flows almost entirely back to the Lender. So, this is the first critical change in the Maple protocol - breaking out the diligence portion of the lending process. Why is this important?

Delegates have skin in the game - literally. Every delegate is required to fund their respective Pool with at least $100,000 worth of Balancer Pool Tokens (BPTs). This acts as cover for any loss of funds in the Pool. In the event of a loan default, the Borrower’s collateral is liquidated first. Since Maple is an undercollateralized lending platform, this is going to end up being a small amount of collateral and likely won’t make up for any major defaults in that Pool. The aforementioned cover is then liquidated to make up as much of the difference as possible, with the goal being to make up lost funds without touching the Lender’s deposits (protecting Lender’s capital is crucial to a healthy system). It’s a bet, required by the Pool’s Delegate, that they will assess their prospective Borrowers well enough so that this cover is highly unlikely to be triggered (otherwise, the Delegate is going to incur losses of their own money).

Again, I’m assuming the reader understands core DeFi concepts, but quickly - BPTs are a tokenized receipt of the quantity of two underlying assets a Delegate has deposited into a Balancer pool. Most DeFi protocols use some equivalent of this; AAVE uses aTokens, AMMs have LP tokens, etc.

In Maple’s case, the specific required pool is MPL:USDC; meaning the Delegate needs to put up at least $50,000 (in the form of USDC) and $50,000 worth of Maple’s governance token, MPL, before they can begin looking for liquidity. I understand this initial design choice by the team, given it 1) incentivizes Delegates but also 2) helps provide liquid markets for people to buy MPL (using USDC).

Delegates are now incentivized to really care about the quality of diligence that goes into reviewing prospective loans. Remember, this is all done transparently on-chain. If I’m a Lender, and I’m looking to deposit some capital into a Maple Pool to earn yield, you can bet I’m not going to give my hard-earned assets to a Delegate with a shoddy track record and high default rate. On top of that, as a Delegate, the money I make is effectively a performance fee. The more liquidity in my Pool, the more loans I can potentially give out, and a healthy loan portfolio means I’m earning a substantial portion of the ongoing fees collected from those loans.

From the Lender’s perspective, the process of earning yield is vastly dumbed down. There is upfront diligence required of the Delegate, but everything else is out of their hands, in return for ~10% of the Ongoing Fees (read: interest payments) received in the Pool. Not a bad trade-off. Delegates are not getting screwed by any means; imagine the magnitude of 10% of all interest accrued by a multi-billion dollar loan portfolio.

Stakers

The second new actor introduced in Maple’s system are Stakers. Stakers do almost the same exact thing as the Delegates - posting cover to a Pool, to earn a higher yield. That yield is higher because Stakers take on a higher level of risk - I mentioned that Maple loans are undercollateralized, so any material default is likely going to trigger the sale of a Pool’s cover, which Stakers are providing. Why would anyone do this, you ask?

Well, let’s say I am a long-term holder of MPL and want to earn some additional yield on that position. I can do some due diligence of my own on the various Delegates in the protocol, find one whose strategy I have conviction in, and post my BPTs as cover to that Pool. I believe this Delegate will run a healthy loan portfolio, and the likelihood of my cover being liquidated to cover losses (the risk) is lower than the return I’m earning.

That return is made up of 10% of all Ongoing Fees in a Pool (this is the recurring Interest payments), as well as MPL rewards that have been reserved for this purpose. More on the MPL token later, but the team is strategically distributing the supply of Maple’s token to incentivize various actors in the system. Some of these pools have <1% coverage, meaning a tiny portion of capital is earning 10% of the entire Pool’s earnings from Ongoing Fees (yeah, I suppose this is almost like a yield farming arb opportunity in Pools with low coverage and high fees).

Example data available on Alameda’s USDC Pool

Right now, the coverage most of the existing pools are seeing is very small - and in some cases consists of not much more beyond the Delegate’s $100,000 requirement. I imagine that this is because that cover (at the moment) only consists of MPL:USDC BPTs. As MPL has skyrocketed in recent months, impermanent loss has been heavy for some early LPs in those Balancer pools. I expect the rate of coverage to increase substantially as single-sided coverage using other tokenized assets becomes available in the future (e.g. WETH, WBTC).

Benefits to Borrowers and Lenders

We have discussed the two new actors in the Maple marketplace, but let’s talk about how the mechanism benefits existing actors in a myriad of ways (when compared to tradfi).

For the Borrower:

“Transparent and efficient financing completed entirely on-chain”, quoted straight from the Maple docs. Borrowers can see what other Borrowers are paying, what their terms are, etc. No more bouncing between meetings with Lenders trying to game your way to the best possible terms by pitching one bank’s term sheet against another’s. Transparency in the market leads to cheaper financing costs across the board on top of saving everyone’s time.

I’ve been thinking about just how efficient this new borrowing process could be in the long run. Due to its immutable nature, anyone can view historical transactions on the Ethereum blockchain at any time, forever. Theoretically, we could reach a point where Borrowers have enough on-chain evidence of high performing loans (e.g. no defaults, years of on-time interest payments), that the diligence/underwriting process might be nearly instantaneous. I can remember how much time we would spend underwriting loans for Borrowers who had already been long time clients, to come to the same conclusion we always did; this Borrower is deserving of our capital, and highly likely to pay us back. This type of stuff is why DeFi is so promising. The step jumps in efficiency gains are going to be insane.

No risk of being margin called or liquidated (unless they default on payments). Because Maple is a series of smart contracts acting as law, there are only a few ways that the Borrower can get liquidated, and it would have to be their own doing. Given these loans on Maple are undercollateralized, it’s not a material amount of funds compared to the loan size overall, anyways. The fear of being margin called is always present in tradfi, and is a massive headache for Borrowers (particularly if they have yet to see the returns of their investments yet, and don’t have capital to meet that margin call). The Delegate entered into a binding agreement with the Borrower, so it’s refreshing to see the Borrower can only effectively be “punished” due to their own mistakes.

For the Lender:

Vastly reduces the overhead with earning a return on capital, without a massive increase in risk. Risk here is now i) counterparty risk that the Delegate will give out bad loans, but I’ve talked about how Delegates are incentivized not to do so, and ii) smart contract risk, but as Ethereum/Maple become more Lindy, I expect this to dissipate over time.

No ongoing maintenance necessary with your capital, which auto-compounds as it earns Ongoing Fees. And while of course there are intelligent controls around how/when Lenders can withdraw their capital, they can claim interest/rewards at any time. It is hands-off to the point that it becomes a fixed-income solution.

Comfort in knowing that Borrowers and Delegates are always KYC/AML approved by the Maple team, so they can rest assured they are not indirectly lending money to a shady actor or a criminal enterprise (shoutout Sifu). While the uncertainty around regulation looms large over the industry, this is the single critical piece that most DeFi applications are missing right now, in terms of getting big tradfi players to make the switch.

Additional benefits of the Maple platform

There are additional benefits to Maple’s platform beyond just the smoother/more transparent lending/borrowing processes for all parties involved.

Undercollateralized Lending - the Holy Grail

While dapps like Aave and Compound were groundbreaking, DeFi hasn’t been able to figure out undercollateralized loans just yet. With those “DeFi 1.0” protocols, users would supply X amount of assets, and be able to borrow Y% of that X value at any given time. Deposit $100, borrow, say $60 against that. Now that’s changed with the advent of Maple’s undercollateralized loans. They are a critical part of capital markets (and any growing, healthy economy), because not every individual/business has the capital to lock away upfront in order to get access to much needed financing. With Maple’s model, firms can access financing with very little (or no) collateral required. I argue the whole DeFi space will mature faster now that solutions like Maple are available.

While other dapps are branching out towards permissioned pools aimed at tradfi (e.g. Aave Arc), the undercollateralized nature of Maple is the differentiator here. Banks can participate in DeFi while only having to put a small amount of capital at risk as collateral.

Scalable

Maple’s design is inherently scalable, as are most decentralized systems. As demand grows for financing on-chain, the number of Pools and Delegates will also grow. It’s easy to envision a future where different banks with different risk tolerances can survey hundreds of Delegates and choose the Pool that most fits their criteria (from either a borrowing or lending perspective). I can remember times as an underwriter where we were turning away loan requests from prospective Borrowers, not because of their financial health, but because we simply couldn’t get to all of them in time. Maple will scale as institutions scale on-chain with DeFi.

Sustainable and realistic yields

Yuga wrote a great overview of where DeFi yields come from in the article below, but the bottom line is that DeFi yields across the board (at least, to an outsider) appear murky and suspicious. At this point in time, most people have accepted that eye-popping yields originate from unsustainable token emissions (sorry, OHM forks, that 11 digit APY is vapor). Most DeFi yields are based off pure speculation, apart from select mechanisms like CRV emissions which act as a (pretty brilliant) way of sourcing liquidity. In the Maple platform, yields are transparent and sustainable, coming from interest paid by firms which are borrowing to grow their business. They are paying interest to access this financing. In other words, that yield is a direct result of growing DeFi as a whole, which is awesome.

Open Source / Inclusive

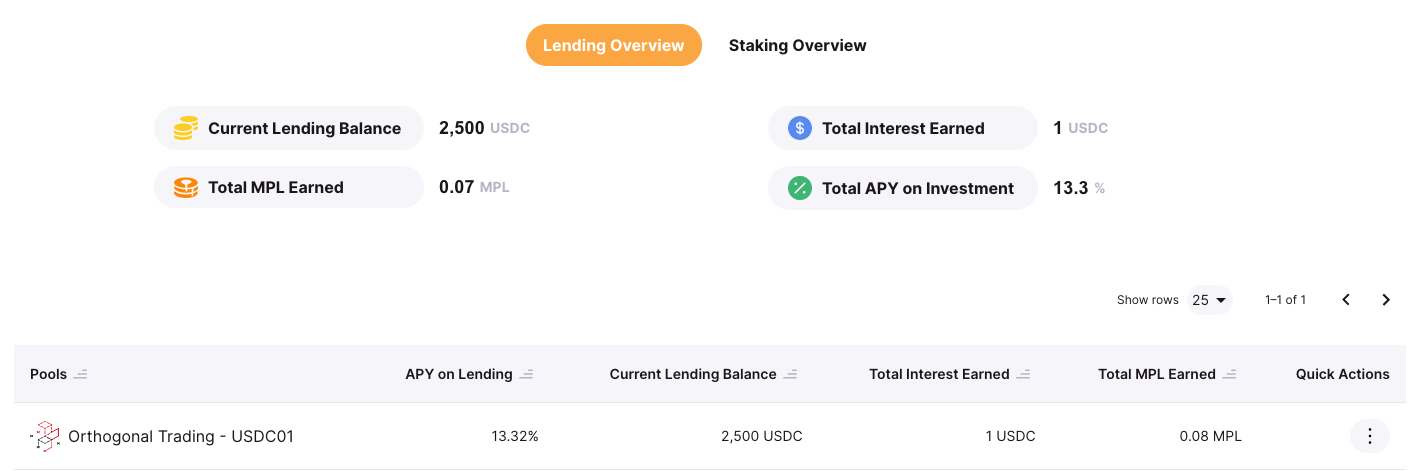

Of course, it is hard to be a huge proponent of DeFi and not mention how the little guy gets a share of the action too. While many of the Pools in the Maple platform are permissioned (you must fulfill certain characteristics in order to participate as a Lender/Borrower), some are permissionless. I’m just a retail investor, yet within a few minutes was able to supply some USDC to Orthogonal Trading’s pool at ~13% APY (see below). Imagine keeping your cash in a traditional savings account…

I’m rich!

Maple has created the means for credit experts to build their own lending platform - leveraging their experience and reputation to attract capital, and maintaining control over who that capital gets loaned out to.

Legitimizing DeFi in the Eyes of the Institutions

There are a few major reasons why tradfi, for the most part, has failed to understand or get involved with the early days of DeFi. In addition to 12 figure APYs on the latest OHM fork, we have a new $100mm+ hack each week, criminal founders of exchanges coming back to life, and so on. I’m getting exhausted just thinking about how fast narratives change on CT.

On top of the fact that this is experimental tech, the other reasons are primarily related to regulation - and as unclear/unhelpful as the US government has been, those guidelines will come eventually. Banks don’t dare touch the permissionless nature of DeFi while these regulations remain unclear, because they are required to care about KYC/AML. I’m a huge proponent of individual privacy, but I’m also a realist. If you want tradfi money to come into crypto, you must maintain some of the same boundaries that they follow today. This is what makes Maple so fundamentally different from most dapps in DeFi. They have built a platform that offers all the benefits of DeFi we’ve talked about, while providing an opportunity for banks to understand and feel comfortable participating in. On top of all major parties being KYC’d, there are also legal outlets for financing that goes south - you know how much banks care about protecting their capital, and that’s not going to change anytime soon. You lie to the Delegate during the diligence process, your ass is getting sued!

So, what’s to stop a JP Morgan from eventually taking some of their credit folks to get whitelisted as a Delegate, and using their own assets to fund said Pool? Considering that these Pools can be permissioned (again, restricting who can Lend and Borrow from them), they still maintain the tight grip on their lending practice. They still get to know who they are lending to, for what reason, negotiate the facility terms, etc. To me, it’s a matter of when a big bank does this via Maple, not if.

MPL Token

So far, I’ve really only focused on how Maple’s platform works, and why it was designed to bring the benefits of DeFi to tradfi, along with some of the standard checks and balances in that system. But it would be a big miss to not talk about their native ERC-20 governance token, MPL, and the ability to actually own a piece of the protocol. It serves a few different purposes:

Governance

As with many early DeFi protocols, Maple utilizes a Governor account that manages Maple’s Treasury, has the power to pause certain aspects of the protocol, and so on (right now, that account is managed via multisig wallet). I am a big proponent of this model in the early days, and don’t think I need to dive into that too much. There are simply too many things that can go wrong this early on. Over the coming years, Maple is going to transition to a fully decentralized governance, at which point MPL holders will hold proportionate voting power based on the % of the total 10,000,000 MPL supply that they hold.

What will they get to vote on? Well, it remains to be seen, as anyone can theoretically propose any change to a DeFi protocol. Some things will be obvious. There are parameters in the protocol that are flexible and subject to updates via approved proposals, including liquidity cap in a given Pool, which addresses can access/interact with a specific Pool, etc. As the Maple protocol iterates and grows, it will eventually have far more flexibility in terms of what can be changed in a given Pool or Loan. Different actors (Delegates, Lenders, Borrowers, Stakers) wanting to influence the direction of these changes will need to hold MPL to vote. Borrowers might want to reduce the Establishment (upfront) Fee, while Stakers may want a higher portion of Ongoing Fees coming their way.

A long-term holder who might not want to get involved in the minutiae of protocol parameters will eventually be able to accept bribes for their votes in a similar mechanism to Convex/Votium. It remains to be seen what voter participation looks like as DeFi matures, but knowing human nature I am pretty confident it will be on the lower end. Firms having a bribing mechanism for otherwise wasted votes makes sense for both sides.

Sharing in platform revenue

Here we go, the most important aspect of Maple’s platform over the long term. At the end of the day, Maple is a revenue generating business. All Borrowers pay a 1% Establishment Fee (basically, an upfront fee, or origination fee, in tradfi terms) on all newly issued loans. 2/3 of this fee, or 0.66% of every issued loan, goes into the Maple Treasury - to be shared proportionately by MPL tokenholders. This was a recent vote that passed, and upgrades to the tokenomics are coming soon. The specific mechanism in which this will occur is similar to the one popularized by Sushiswap, via xSushi.

Users can lock MPL tokens into the protocol to receive xMPL, and that revenue I mentioned earlier goes towards buying back MPL in the open market and distributing it to xMPL holders (so you are earning more MPL as the protocol grows). Theoretically, this functions similarly to stock buybacks in tradfi, which normally equate to price appreciation.

Side note: this will help alleviate one of the main complaints currently coming from MPL holders, which is heavy impermanent loss in the MPL:USDC pools that Delegates and Stakers use. The introduction of single-sided staking allows users to share in the platform’s loan growth while avoiding impermanent loss. In DeFi, users want to earn yield on their tokens, but not when that token is getting crushed in a USDC Balancer pool.

Future Utility

xMPL (the tokenized receipt of how much MPL you have locked into the protocol) will eventually be eligible to be staked as cover to a given Pool. Another source of yield, without the potential for impermanent loss, for those willing to take on a bit more risk on behalf of Lenders in a Pool.

Even more importantly, there have been discussions around incentivizing Borrowers to hold meaningful amounts of MPL in return for rebates on interest paid. Yes, this means that the Alameda’s of the world, who are using Maple for financing, will be able to get cheaper financing in the future by buying MPL. Crypto as an asset class will keep growing at a rapid pace, and these firms will grow concurrently, needing capital to do so. Combined with the ability to vote on the direction of the protocol, this leads me to believe we are going to see (are maybe already seeing, given MPL’s market outperformance recently) a CRV Wars style accumulation battle for the MPL supply.

What’s next for Maple

Grow, grow, grow

The infrastructure is in place, and existing Borrowers like Alameda are beginning to ramp up their drawdowns as both parties gain comfort with each other (Borrowers establishing a track record, Maple establishing itself as somewhat Lindy). Outstanding loans are creeping up to the billy mark in roughly 10 months, and the team is targeting $5bn in TVL by the end of 2022. We’ve crossed the threshold where crypto is no longer a consensus scam - it is the fastest growing asset class in history and that does not appear to be slowing down any time soon. Maple will grow rapidly right alongside it.

via Maple’s Dune Analytics page

Maple Solana and $SYRUP (🥞🥞🥞)

Solana will be the first alt-L1 that Maple launches its platform on (following the acquisition of the Avari team a few months back). Given that Solana, with its focus on high throughput and performance, is catering towards the financial sector, an undercollateralized lending platform will be crucial to growing that ecosystem (making it highly valuable). This is a no-brainer move for Maple to become multi-chain and it should be launching in the next few weeks. How long until Jump gets financing through Maple Solana? (I’d bet they are one of the first Borrowers once it goes live).

To add on to the section above on MPL utility, 40% of the total supply of $SYRUP (the token for Maple Solana) will be owned by the Maple Treasury. So yeah, owning MPL means you’re already going to share in the success (and direction) of DeFi on Solana.

Protocol Upgrades

Over time, Maple’s smart contract functionality will only become more flexible. The v2 docs point towards refinancing, for example, but we’re only just beginning to scratch the surface of composability in DeFi. I personally get excited about the thought of:

Earning yield with Borrowers’ locked collateral, instead of sitting idly

Earning yield with excess liquidity in a given Pool, at the Delegate’s discretion

Tokenized assets as Pool cover (e.g. you can earn a return, including MPL rewards, by staking WETH, WBTC, etc.)

Increased complexity in loan terms, maybe even different categories of loans. Every Borrower has a different need, and as an underwriter no two loans were identical. Loans collateralized by a startup founder’s tokens, for example.

New Target Borrowers

The team has spoken publicly about this, but they plan to branch out into offering undercollateralized financing on their platform to far more than just cryptonative hedge funds and market makers. The obvious next step is crypto mining companies, as an increasing portion of the BTC hash rate moves into the US - and those companies must be some of the hungriest for capital in the industry. You can never have enough computers chomping away mining BTC in Texas. Plus, they have (relatively) predictable revenue streams for years to come. SaaS and other tech companies come next, but the ultimate goal is the tradfi institutional money. Bulge bracket banks dipping their toes in DeFi via Maple will be the catalyst for trillions of dollars transitioning over to this new system.

Thinking Bigger

Imagine modifying the Maple protocol design for the traditional Venture Capital model, for example. LPs fund Pools run by Delegates who consist of VC/angel investors with an on-chain portfolio of investments and returns to attract capital.

Eventually I can see nascent DeFi protocols using Maple for fueling growth as opposed to expensive and dilutive liquidity mining programs. We’ve seen so many successful dapps grow rapidly without access to undercollateralized loans already - that number will only accelerate moving forward. Imagine these loans are secured by the new protocol’s native token as collateral. Or the design gets flexible enough to allow Delegates to receive a portion of future revenue in exchange for interest free financing.

There are so many possibilities of how Maple will eventually take shape and help crypto and DeFi grow as an industry. Shit, Maple might end up indirectly creating a whole consulting industry of blockchain engineers who are hired by Borrowers/Lenders to facilitate the on-chain portion of the Maple process. I laugh thinking about a bunch of suits in a high rise trying to figure out how to call smart contracts.

Conclusion

I am predicting that Maple will have onboarded at least 1 Delegate and 1 Borrower from any of the major bulge-bracket banks by 2025 - opening the floodgates for that institutional capital to join this wild DeFi experiment (of course, this is assuming the regulation stuff gets figured out). Eventually tens or hundreds of billions in loans will have been made through the Maple protocol, earning revenue for its MPL tokenholders. Suffice to say I am excited to see where things go next.

Mac